Thought Leadership

Cross a Border, Lose a Decade

May 14, 2026

Written by: Kevin Lehtiniitty & John Onwualu

A merchant in São Paulo can receive payment from a customer anywhere in Brazil in under two seconds, for free, thanks to PIX. Brazil built PIX in 2020. Five years later, it has 170 million users and processes more transactions than Visa and Mastercard combined within the country.

Now send that same payment to a supplier in Lagos, and it enters a system designed in 1973. It bounces through two or three correspondent banks, loses 3 to 5 percent to fees and foreign exchange markups, and arrives in two to five business days if nothing goes wrong. The most common customer service request at major international banks is still, after fifty years: where is my wire? The industry spends more than $2 billion per year just investigating that question.

Both countries have real-time domestic payment infrastructure. So do more than 80 others. India's UPI processes 228 billion transactions a year, more daily volume than Visa handles globally. Europe's SEPA Instant covers 36 countries with a regulatory mandate for universal adoption. Mexico's SPEI handles 5 billion payments annually. Thailand's PromptPay has registered 70 million IDs in a country of 72 million. Nigeria's NIP processes over a billion transactions per quarter.

All of them settle in seconds. All of them run 24/7. We have, more or less, solved domestic payments.

But none of these systems talk to each other. Cross a border and you fall back into infrastructure from a different era. Two previous generations of solutions hit the same ceiling, and we believe we're on the verge of a third era where a real solve is possible. Stablecoins cracked the settlement layer, but the missing piece isn't better rails. It's the orchestration network that connects them all. Fast, cheap, invisible.

Payments 1.0: The Correspondent Banking Era

We think of the first generation as the Correspondent Banking era. A SWIFT message hops through a chain of correspondent banks. Each hop adds compliance screening, FX conversion, and fees. Settlement takes 2–5 business days. The system relied on traditional banks and cost a fortune:

6.49% average remittance fee

13.64% through banks specifically

FX spreads buried in rates (~$3,000 on a $100K transfer vs. $25 explicit fee)

$27 trillion globally tied up in pre-funded nostro/vostro accounts

Correspondent banking is not a conspiracy. It is an equilibrium that persists because replacing it means disrupting every participant's business model simultaneously. It was a reasonable design for a world where cross-border commerce was the exception. It is an unreasonable one for a world where it is the norm.

Payments 2.0: The Fintech Ceiling

The second generation delivered a genuine revolution in customer experience. Companies like Wise, Nium, Airwallex, and Thunes looked at the correspondent banking chain and asked a simple question: what if we built our own network?

These companies pre-funded local accounts in 50+ countries. Money never actually crosses borders because funds are collected locally on one side and disbursed locally on the other. This solves the expensive FX conversion and correspondent banking costs only to replace them with capital costs. Wise’s ~0.53% per transfer is 10× cheaper than banks but they need enormous capital reserves and revolving credit facilities.

Two models, two unsatisfactory solutions. Moreover, the corridors that need improvement most - between fast-growing economies in Africa, Latin America, and Southeast Asia - are exactly the ones that neither model can reach effectively.

Central banks see the gap. The Bank for International Settlements launched Project Nexus to interconnect domestic real-time payment systems directly. Central bank digital currencies aim to modernize sovereign money for cross-border use. These are serious efforts by serious institutions.

But they share a constraint: they require multilateral coordination between central banks with different regulatory frameworks, different monetary policies, different data sovereignty requirements, and different political timelines. Project Nexus will not go live until 2027 at the earliest, and only for five countries. Scaling to 80 systems is a multi-decade proposition. CBDCs, by design sovereign and fragmented, recreate at the protocol level the same interoperability problem they intend to solve. A digital euro and a digital yuan do not automatically talk to each other any more than SEPA and SPEI do today.

We need something else. Enter Payments Era 3.0.

Payments 3.0: The Missing Bridge

Stablecoin infrastructure offers a different path. Not replacing local currencies. Not replacing domestic payment systems. Not replacing banks. Connecting all of them.

The architecture is straightforward. A company in Mexico initiates a payment through its local bank or fintech. Mexican pesos convert to a dollar-denominated stablecoin through a licensed local provider, using Mexico's existing domestic rails. That stablecoin settles on a blockchain in under a second. At the destination, a licensed Kenyan provider converts the stablecoin to Kenyan shillings and deposits them into the supplier's account through Kenya's NIP system.

Two domestic transactions, each using the real-time rails the country already built. One cross-border hop on a blockchain. No correspondent banks. No nostro accounts. No four-institution chain. No "where is my wire?"

The domestic legs of this transaction use the banking systems countries have already invested in. Stablecoins do not eliminate banks. They eliminate the need for banks to maintain bilateral correspondent relationships across every border. The domestic banking system becomes the last mile, which is exactly what it is good at. The stablecoin replaces only the part that is broken: the cross-border hop.

This changes more than speed. It changes the entire capital structure of cross-border payments. Because settlement happens in real time, there is no need to pre-fund accounts around the world.

But real-time settlement, by itself, does not solve the problem. It solves the plumbing. The harder challenge is everything around it.

Consider what happens when a business needs to move value from Mexico to Kenya on stablecoin rails. Which provider handles the peso on-ramp? Which handles the shilling off-ramp? If there are three licensed providers in Kenya, one with tight spreads on transactions under $10,000, another with better rates on large transfers but a four-hour settlement window, and a third that covers the corridor only during Nairobi business hours, who selects the best route? If the first provider goes offline mid-transaction, who reroutes to the second without the sender knowing? If Mexican compliance requires one data format and Kenyan compliance requires another, who normalizes them?

These problems are the daily operational reality of a fragmented provider ecosystem. Stablecoins created a new settlement layer. What they did not create is a network. Dozens of licensed providers now operate across these regions, but each covers different corridors with different capabilities, different APIs, different rate refresh cycles, and different compliance frameworks. Without a coordination layer, a business trying to use stablecoin infrastructure faces the same bilateral integration problem that Payments 2.0 was supposed to fix: connect to each provider individually, manage each relationship, monitor each corridor, handle each failure mode. One integration becomes twelve. The front end changed. The scaling problem did not.

The missing piece is orchestration. A neutral network layer that connects to licensed providers across jurisdictions, routes transactions to the best available path, manages compliance across corridors, and gives the sender a single integration point instead of dozens. The settlement layer is the railroad. The network layer is the switching system that makes the railroad useful.

Neutrality here is an economic mechanism, not an idealogy. When multiple independent providers compete on the same corridor through a neutral layer, pricing compresses. When a single issuer or provider controls the network, they optimize for their own corridors, their own liquidity, their own economics. The corridors that need improvement most are the ones no single provider can serve profitably alone. A neutral layer that aggregates providers and lets them compete on equal terms is the only architecture that drives pricing toward parity across every corridor.

The performance difference is not incremental. A correspondent banking wire takes days, and its real cost is not the $25 wire fee but the FX markups, intermediary charges, and pre-funded capital that make the whole chain possible. A stablecoin transfer replaces that entire cost structure: one FX conversion at origin, real-time settlement at a fraction of a cent, one FX conversion at destination. Two transparent conversions instead of two opaque ones, with no intermediary extracting rent in between.

The Evidence

Claims about infrastructure transitions are easy to make. Data is harder to argue with.

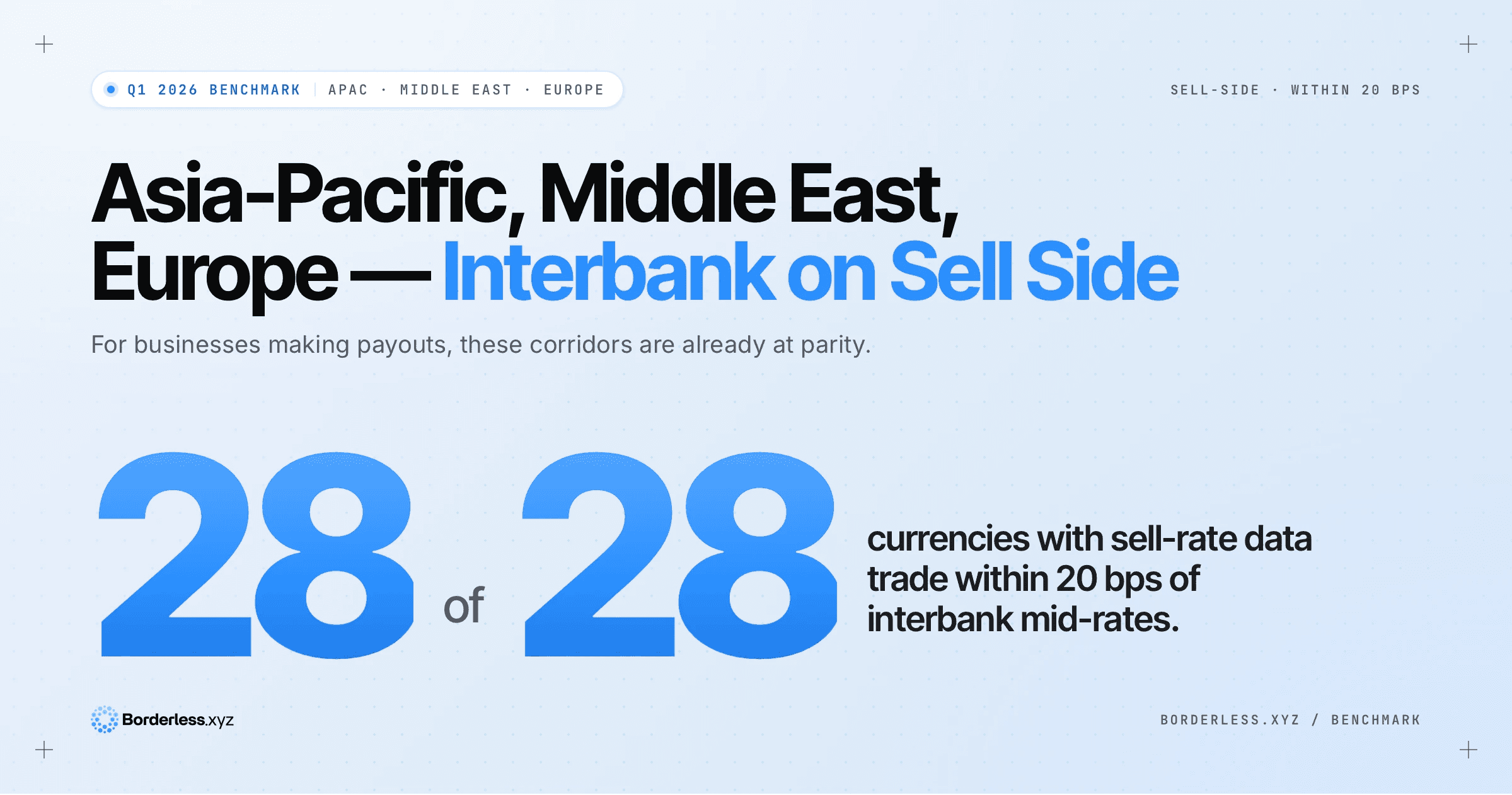

The Borderless Stablecoin FX Benchmark tracks live exchange rates across 51 stablecoin-to-fiat currency pairs, sourced from multiple independent providers operating on the Borderless network. In Q1 2026, the benchmark captured 1.15 million rate observations across 90 calendar days. This is observed pricing on live infrastructure. The findings, broken down by region:

Not every corridor is there yet, and honesty about that matters. Frontier currencies with thin liquidity and capital controls like the Ghanaian cedi, the Malawian kwacha, and the Congolese franc, remain expensive on stablecoin rails, just as they are on traditional rails. In some cases, the "premium" reflects parallel market dynamics: stablecoins price at the rate businesses actually pay on the ground, not the official rate published by a central bank managing capital controls. The gap is real, but it is a gap of market structure, not technology.

The trajectory tells the rest of the story. Today's expensive African corridors look like Latin American corridors did eighteen months ago. As more providers enter, as liquidity deepens, as volume grows, pricing compresses. The pattern is consistent across every corridor that has moved from single-provider to multi-provider coverage.

What Comes Next

Three forces are converging that make this transition unavoidable.

The first is capital. Visa, Mastercard, and Stripe have collectively deployed more than $4 billion in stablecoin acquisitions and infrastructure in the last 18 months. That capital is not speculative. It is building rails, acquiring licenses, and integrating with domestic payment systems country by country. When the largest payments companies in the world invest at that scale, they are not making a bet on a trend. They are building the next generation of their own infrastructure.

The second is regulation. The GENIUS Act did not just legalize stablecoins. It created the compliance framework that institutional adopters need before they will route real volume through new rails. Reserve requirements, audit mandates, and issuer licensing give a Fortune 100 CFO the same regulatory clarity on stablecoins that they have on card networks. That clarity is what converts institutional interest into institutional adoption.

The third is gravity. Every corridor that moves from single-provider to multi-provider coverage follows the same pattern: pricing compresses toward interbank parity. Latin America is already there. East Africa is compressing in real time. As the neutral network layer connects more providers to more corridors, the economics become self-reinforcing. Better pricing attracts more volume. More volume attracts more providers. More providers compress pricing further.

The end state is invisible infrastructure. The sender will see their local currency. The receiver will see theirs. Neither will know or care that a stablecoin was involved. The most important infrastructure is the kind people forget is there.

Kevin Lehtiniitty is CEO and co-founder of Borderless.xyz, a stablecoin infrastructure platform connecting wallet providers to licensed payment partners across 95+ countries. John Onwualu is at Flourish Ventures, an $850 million global fund investing in financial technology. Both have financial interests in the stablecoin infrastructure ecosystem. The Borderless Stablecoin FX Benchmark data cited in this piece is derived from live rate observations on the Borderless network and is available for review.

Key Sources

Cross-border payment costs: World Bank, Remittance Prices Worldwide (2025)

Nostro/vostro capital ($27T): McKinsey, Global Payments Report; Convera

Correspondent banking contraction: BIS, Correspondent Banking Data (2019, 2020)

Payment investigation costs ($2B/year): SWIFT

Remitly pre-funding: Remitly 8-K and 10-Q filings, SEC EDGAR (2025)

Stablecoin FX rates: Borderless, "Borderless Benchmark Quarterly Insights — Q1 2026" (1.15M rate observations, 51 currencies)

GENIUS Act: Congress.gov; Morgan Lewis (2025)

Stablecoin Treasury holdings ($150B+): a16z, State of Crypto Report (2025)

Federal Reserve stablecoin research: FEDS Notes, "Payment Stablecoins and Cross-Border Payments" (March 2026)

A merchant in São Paulo can receive payment from a customer anywhere in Brazil in under two seconds, for free, thanks to PIX. Brazil built PIX in 2020. Five years later, it has 170 million users and processes more transactions than Visa and Mastercard combined within the country.

Now send that same payment to a supplier in Lagos, and it enters a system designed in 1973. It bounces through two or three correspondent banks, loses 3 to 5 percent to fees and foreign exchange markups, and arrives in two to five business days if nothing goes wrong. The most common customer service request at major international banks is still, after fifty years: where is my wire? The industry spends more than $2 billion per year just investigating that question.

Both countries have real-time domestic payment infrastructure. So do more than 80 others. India's UPI processes 228 billion transactions a year, more daily volume than Visa handles globally. Europe's SEPA Instant covers 36 countries with a regulatory mandate for universal adoption. Mexico's SPEI handles 5 billion payments annually. Thailand's PromptPay has registered 70 million IDs in a country of 72 million. Nigeria's NIP processes over a billion transactions per quarter.

All of them settle in seconds. All of them run 24/7. We have, more or less, solved domestic payments.

But none of these systems talk to each other. Cross a border and you fall back into infrastructure from a different era. Two previous generations of solutions hit the same ceiling, and we believe we're on the verge of a third era where a real solve is possible. Stablecoins cracked the settlement layer, but the missing piece isn't better rails. It's the orchestration network that connects them all. Fast, cheap, invisible.

Payments 1.0: The Correspondent Banking Era

We think of the first generation as the Correspondent Banking era. A SWIFT message hops through a chain of correspondent banks. Each hop adds compliance screening, FX conversion, and fees. Settlement takes 2–5 business days. The system relied on traditional banks and cost a fortune:

6.49% average remittance fee

13.64% through banks specifically

FX spreads buried in rates (~$3,000 on a $100K transfer vs. $25 explicit fee)

$27 trillion globally tied up in pre-funded nostro/vostro accounts

Correspondent banking is not a conspiracy. It is an equilibrium that persists because replacing it means disrupting every participant's business model simultaneously. It was a reasonable design for a world where cross-border commerce was the exception. It is an unreasonable one for a world where it is the norm.

Payments 2.0: The Fintech Ceiling

The second generation delivered a genuine revolution in customer experience. Companies like Wise, Nium, Airwallex, and Thunes looked at the correspondent banking chain and asked a simple question: what if we built our own network?

These companies pre-funded local accounts in 50+ countries. Money never actually crosses borders because funds are collected locally on one side and disbursed locally on the other. This solves the expensive FX conversion and correspondent banking costs only to replace them with capital costs. Wise’s ~0.53% per transfer is 10× cheaper than banks but they need enormous capital reserves and revolving credit facilities.

Two models, two unsatisfactory solutions. Moreover, the corridors that need improvement most - between fast-growing economies in Africa, Latin America, and Southeast Asia - are exactly the ones that neither model can reach effectively.

Central banks see the gap. The Bank for International Settlements launched Project Nexus to interconnect domestic real-time payment systems directly. Central bank digital currencies aim to modernize sovereign money for cross-border use. These are serious efforts by serious institutions.

But they share a constraint: they require multilateral coordination between central banks with different regulatory frameworks, different monetary policies, different data sovereignty requirements, and different political timelines. Project Nexus will not go live until 2027 at the earliest, and only for five countries. Scaling to 80 systems is a multi-decade proposition. CBDCs, by design sovereign and fragmented, recreate at the protocol level the same interoperability problem they intend to solve. A digital euro and a digital yuan do not automatically talk to each other any more than SEPA and SPEI do today.

We need something else. Enter Payments Era 3.0.

Payments 3.0: The Missing Bridge

Stablecoin infrastructure offers a different path. Not replacing local currencies. Not replacing domestic payment systems. Not replacing banks. Connecting all of them.

The architecture is straightforward. A company in Mexico initiates a payment through its local bank or fintech. Mexican pesos convert to a dollar-denominated stablecoin through a licensed local provider, using Mexico's existing domestic rails. That stablecoin settles on a blockchain in under a second. At the destination, a licensed Kenyan provider converts the stablecoin to Kenyan shillings and deposits them into the supplier's account through Kenya's NIP system.

Two domestic transactions, each using the real-time rails the country already built. One cross-border hop on a blockchain. No correspondent banks. No nostro accounts. No four-institution chain. No "where is my wire?"

The domestic legs of this transaction use the banking systems countries have already invested in. Stablecoins do not eliminate banks. They eliminate the need for banks to maintain bilateral correspondent relationships across every border. The domestic banking system becomes the last mile, which is exactly what it is good at. The stablecoin replaces only the part that is broken: the cross-border hop.

This changes more than speed. It changes the entire capital structure of cross-border payments. Because settlement happens in real time, there is no need to pre-fund accounts around the world.

But real-time settlement, by itself, does not solve the problem. It solves the plumbing. The harder challenge is everything around it.

Consider what happens when a business needs to move value from Mexico to Kenya on stablecoin rails. Which provider handles the peso on-ramp? Which handles the shilling off-ramp? If there are three licensed providers in Kenya, one with tight spreads on transactions under $10,000, another with better rates on large transfers but a four-hour settlement window, and a third that covers the corridor only during Nairobi business hours, who selects the best route? If the first provider goes offline mid-transaction, who reroutes to the second without the sender knowing? If Mexican compliance requires one data format and Kenyan compliance requires another, who normalizes them?

These problems are the daily operational reality of a fragmented provider ecosystem. Stablecoins created a new settlement layer. What they did not create is a network. Dozens of licensed providers now operate across these regions, but each covers different corridors with different capabilities, different APIs, different rate refresh cycles, and different compliance frameworks. Without a coordination layer, a business trying to use stablecoin infrastructure faces the same bilateral integration problem that Payments 2.0 was supposed to fix: connect to each provider individually, manage each relationship, monitor each corridor, handle each failure mode. One integration becomes twelve. The front end changed. The scaling problem did not.

The missing piece is orchestration. A neutral network layer that connects to licensed providers across jurisdictions, routes transactions to the best available path, manages compliance across corridors, and gives the sender a single integration point instead of dozens. The settlement layer is the railroad. The network layer is the switching system that makes the railroad useful.

Neutrality here is an economic mechanism, not an idealogy. When multiple independent providers compete on the same corridor through a neutral layer, pricing compresses. When a single issuer or provider controls the network, they optimize for their own corridors, their own liquidity, their own economics. The corridors that need improvement most are the ones no single provider can serve profitably alone. A neutral layer that aggregates providers and lets them compete on equal terms is the only architecture that drives pricing toward parity across every corridor.

The performance difference is not incremental. A correspondent banking wire takes days, and its real cost is not the $25 wire fee but the FX markups, intermediary charges, and pre-funded capital that make the whole chain possible. A stablecoin transfer replaces that entire cost structure: one FX conversion at origin, real-time settlement at a fraction of a cent, one FX conversion at destination. Two transparent conversions instead of two opaque ones, with no intermediary extracting rent in between.

The Evidence

Claims about infrastructure transitions are easy to make. Data is harder to argue with.

The Borderless Stablecoin FX Benchmark tracks live exchange rates across 51 stablecoin-to-fiat currency pairs, sourced from multiple independent providers operating on the Borderless network. In Q1 2026, the benchmark captured 1.15 million rate observations across 90 calendar days. This is observed pricing on live infrastructure. The findings, broken down by region:

Not every corridor is there yet, and honesty about that matters. Frontier currencies with thin liquidity and capital controls like the Ghanaian cedi, the Malawian kwacha, and the Congolese franc, remain expensive on stablecoin rails, just as they are on traditional rails. In some cases, the "premium" reflects parallel market dynamics: stablecoins price at the rate businesses actually pay on the ground, not the official rate published by a central bank managing capital controls. The gap is real, but it is a gap of market structure, not technology.

The trajectory tells the rest of the story. Today's expensive African corridors look like Latin American corridors did eighteen months ago. As more providers enter, as liquidity deepens, as volume grows, pricing compresses. The pattern is consistent across every corridor that has moved from single-provider to multi-provider coverage.

What Comes Next

Three forces are converging that make this transition unavoidable.

The first is capital. Visa, Mastercard, and Stripe have collectively deployed more than $4 billion in stablecoin acquisitions and infrastructure in the last 18 months. That capital is not speculative. It is building rails, acquiring licenses, and integrating with domestic payment systems country by country. When the largest payments companies in the world invest at that scale, they are not making a bet on a trend. They are building the next generation of their own infrastructure.

The second is regulation. The GENIUS Act did not just legalize stablecoins. It created the compliance framework that institutional adopters need before they will route real volume through new rails. Reserve requirements, audit mandates, and issuer licensing give a Fortune 100 CFO the same regulatory clarity on stablecoins that they have on card networks. That clarity is what converts institutional interest into institutional adoption.

The third is gravity. Every corridor that moves from single-provider to multi-provider coverage follows the same pattern: pricing compresses toward interbank parity. Latin America is already there. East Africa is compressing in real time. As the neutral network layer connects more providers to more corridors, the economics become self-reinforcing. Better pricing attracts more volume. More volume attracts more providers. More providers compress pricing further.

The end state is invisible infrastructure. The sender will see their local currency. The receiver will see theirs. Neither will know or care that a stablecoin was involved. The most important infrastructure is the kind people forget is there.

Kevin Lehtiniitty is CEO and co-founder of Borderless.xyz, a stablecoin infrastructure platform connecting wallet providers to licensed payment partners across 95+ countries. John Onwualu is at Flourish Ventures, an $850 million global fund investing in financial technology. Both have financial interests in the stablecoin infrastructure ecosystem. The Borderless Stablecoin FX Benchmark data cited in this piece is derived from live rate observations on the Borderless network and is available for review.

Key Sources

Cross-border payment costs: World Bank, Remittance Prices Worldwide (2025)

Nostro/vostro capital ($27T): McKinsey, Global Payments Report; Convera

Correspondent banking contraction: BIS, Correspondent Banking Data (2019, 2020)

Payment investigation costs ($2B/year): SWIFT

Remitly pre-funding: Remitly 8-K and 10-Q filings, SEC EDGAR (2025)

Stablecoin FX rates: Borderless, "Borderless Benchmark Quarterly Insights — Q1 2026" (1.15M rate observations, 51 currencies)

GENIUS Act: Congress.gov; Morgan Lewis (2025)

Stablecoin Treasury holdings ($150B+): a16z, State of Crypto Report (2025)

Federal Reserve stablecoin research: FEDS Notes, "Payment Stablecoins and Cross-Border Payments" (March 2026)

Global Stablecoin Orchestration Network

Borderless Innovations Labs Inc. (Borderless) is a technology and smart contract development company. Borderless in not a broker-dealer or financial institution and does not engage any conduct or transactions requiring such registration. All financial products are offered by and through financial institutions directly. Borderless does not make any recommendation for the purchase or sale of digital assets. Our products and services are offered in limited jurisdictions so please contact our partnerships team for further information and refer to our Terms of Services.

Global Stablecoin Orchestration Network

Borderless Innovations Labs Inc. (Borderless) is a technology and smart contract development company. Borderless in not a broker-dealer or financial institution and does not engage any conduct or transactions requiring such registration. All financial products are offered by and through financial institutions directly. Borderless does not make any recommendation for the purchase or sale of digital assets. Our products and services are offered in limited jurisdictions so please contact our partnerships team for further information and refer to our Terms of Services.

Global Stablecoin Orchestration Network

Borderless Innovations Labs Inc. (Borderless) is a technology and smart contract development company. Borderless in not a broker-dealer or financial institution and does not engage any conduct or transactions requiring such registration. All financial products are offered by and through financial institutions directly. Borderless does not make any recommendation for the purchase or sale of digital assets. Our products and services are offered in limited jurisdictions so please contact our partnerships team for further information and refer to our Terms of Services.