Thought Leadership

The Stablecoin Skyscanner

Written by: Kevin Lehtiniitty & Christopher Grilhault des Fontaines

You know how to move money across borders. You've built payment flows across dozens of corridors, benchmarked providers on total cost and settlement speed, and optimized routing for every market you operate in. You can compare the all-in cost of a payment through one rail versus another in seconds. Cross-border payments are a margin game, and you've spent years learning how to win it.

Stablecoin on/off ramps are a much less mature market. The provider landscape is fragmented, pricing is opaque, and the benchmarking tools that traditional payments teams take for granted are still catching up. Pricing opacity is just the start. The providers themselves are younger, less battle-tested, and building on banking relationships far more fragile than anything on traditional rails. If you're a payments company expanding into stablecoins, the same disciplines apply, but the provider risk profile is nothing like what you're used to.

The Market You Know vs. the Market You're Entering

Traditional cross-border payments run on infrastructure that's been built, rebuilt, and optimized over decades. At the foundation, you have correspondent banking: networks of nostro and vostro accounts where banks pre-fund foreign currency balances so they can settle transactions on each other's behalf. On top of that, you have the networks and platforms that move money at scale. Mastercard Move reaches 10 billion endpoints across 200 countries. Thunes connects over 7 billion mobile wallets and bank accounts across 130 countries. dLocal processes over $9 billion per quarter across 40+ emerging markets. Airwallex handles global FX and payments infrastructure for businesses across 150+ countries.

These are mature rails. If you're a PSP operating in this world, the playbook is straightforward. You pick a provider, commit volume, and negotiate your pricing down. The more volume you bring, the tighter your basis points. It works because the underlying liquidity is deep enough and consolidated enough that a single well-chosen partner can offer competitive rates across most of your corridors. These providers are also stable. Redundant banking relationships. Regulatory frameworks they've operated under for years. Uptime measured in nines. When you commit volume to a Thunes or a dLocal, you're not worried about whether they'll still be able to settle in Brazil next quarter.

Stablecoin on/off ramps work differently.

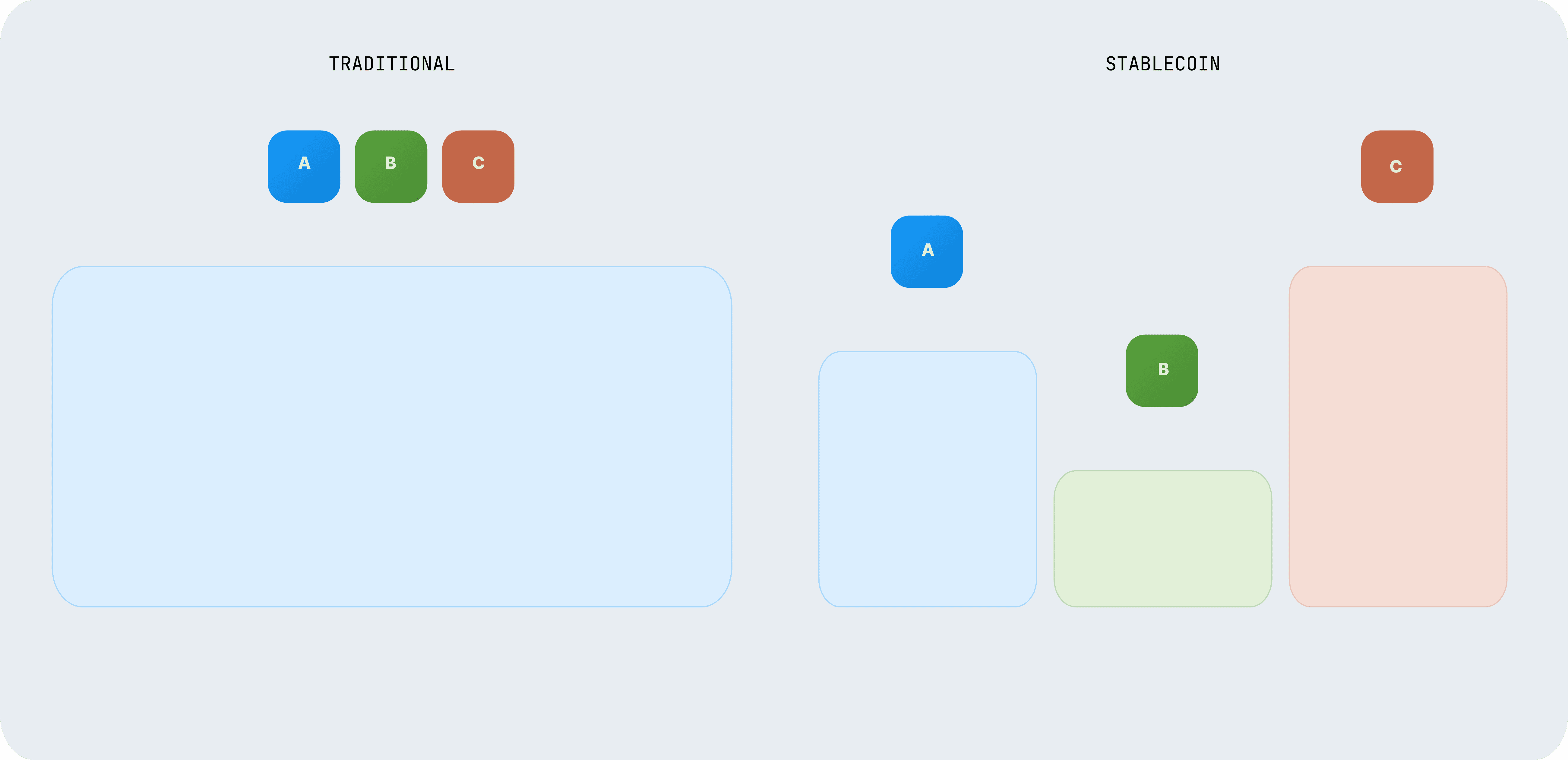

There's no equivalent infrastructure. Instead, there are dozens of regional on-ramp and off-ramp providers, each licensed in specific jurisdictions, each with different banking relationships, and each pricing their FX conversion independently. A provider with deep local bank partnerships in Brazil may have excellent BRL rates but much weaker liquidity in Mexico. Another might offer tight spreads in Kenya but charge a premium in Nigeria.

The pricing fragments. So does the reliability. These are younger companies, and the banking relationships they depend on can break. A local bank that's comfortable handling crypto-to-fiat today might pull back tomorrow — after a regulatory shift, a compliance review, or simply a change in risk appetite at the bank. When that happens, the provider doesn't reprice. The corridor goes dark. In traditional payments, losing a banking partner is a disruption you manage. In stablecoin off-ramps, your payments in that market stop. No notice. No fallback.

And because the market is still in its land-grab phase, providers are competing aggressively for early volume. They'll promise coverage, rates, and capabilities to get you signed. Some will deliver. Some won't. The gap between what's on the pitch deck and what's in production can be significant — and you won't always find out until you're live, volume is flowing, and switching costs are real.

In traditional payments, your disaster recovery plan for a provider outage is straightforward - you have secondary routes, established failover procedures, and providers with the operational depth to recover quickly. In stablecoin payments, if your single provider goes down in a corridor, there's no secondary route. You don't have a warm standby. You have a phone call and a scramble.

The traditional playbook of committing volume to a single provider doesn't solve the problem. The liquidity is too fragmented for any one partner to be consistently competitive across your corridors. And the operational risk of depending on a single, less mature provider — with jurisdiction-specific banking relationships that could change at any time — is a bet most payments teams wouldn't accept on traditional rails. Why accept it here?

We wanted to quantify just how wide the pricing gaps are. So we ran the numbers.

The Data

We analyzed USDC sell rate quotes across 10 licensed providers over a three-month window. Eight corridors: four in Latin America (BRL, MXN, ARS, COP) and four in Africa (GHS, KES, NGN, ZAR). All rates captured at the same timestamps, same notional amounts, providers anonymized.

The median cross-provider dispersion across all eight corridors was 176 basis points. For a PSP routing $5M per month through stablecoin off-ramps, that translates to over $1.2 million per year in avoidable cost from provider selection alone.

Corridor | Spread (bps) | @ $5M/mo | @ $25M/mo | @ $100M/mo |

|---|---|---|---|---|

USDC→GHS | 575 | $3.35M | $16.77M | $67.07M |

USDC→ARS | 394 | $2.32M | $11.59M | $46.37M |

USDC→NGN | 191 | $1.14M | $5.68M | $22.73M |

USDC→MXN | 186 | $1.11M | $5.53M | $22.12M |

USDC→KES | 165 | $0.98M | $4.91M | $19.63M |

USDC→COP | 152 | $0.91M | $4.54M | $18.15M |

USDC→BRL | 65 | $0.39M | $1.96M | $7.82M |

USDC→ZAR | 6 | $0.04M | $0.18M | $0.73M |

Blended avg | 176 | $1.28M | $6.39M | $25.58M |

Per-corridor figures assume full volume in that corridor. Blended average assumes equal distribution across all eight. See Methodology for details.

The range tells its own story. In South Africa, providers largely agree on pricing: 6 bps of dispersion. In Ghana, they don't: 575 bps, nearly a hundred times wider. Even within the same continent, the variation is dramatic. Nigeria (191 bps) looks nothing like South Africa (6 bps). Colombia (152 bps) looks nothing like Brazil (65 bps).

Pricing dispersion is what we can put numbers on. Reliability, settlement consistency, and corridor uptime vary at least as much — they're just harder to put in a table. The corridors with the widest pricing gaps are the same ones where banking relationships are thinnest and providers are most likely to hit disruptions. High dispersion is a maturity signal, not just a pricing one.

But the most important finding isn't the size of the gaps. It's that no single provider wins everywhere.

No single provider consistently offered the best rate across corridors. The best provider in Brazil was different from the best in Colombia, which was different from the best in Argentina. Same story in Africa: the provider with the best rate in Ghana ranked dead last in Kenya. Even a PSP focused on a single region still faces a market where the optimal provider shifts corridor by corridor.

This means static provider routing — picking one partner and sending all volume through them — leaves money on the table regardless of your geographic focus. It also concentrates risk. When your single provider has an outage, loses a banking relationship, or faces regulatory action in a market you depend on, there's no plan B. No failover. No continuity. No single provider is bad. But the market rewards breadth — better pricing, built-in redundancy, and the leverage of not depending on a single vendor's fate. The PSP with that breadth is cheaper, more resilient, and harder to knock offline in every corridor they compete in.

Why the Dispersion Exists

If you're coming from traditional payments, your instinct is to assume this is a temporary inefficiency. That the market will consolidate, a few winners will emerge, and spreads will tighten to the levels you're used to. Eventually, some of that will happen. But the fragmentation in stablecoin on/off ramps isn't a bug. It's structural, and it changes how you approach the market.

In traditional cross-border payments, consolidation happened because the underlying infrastructure allowed it. Correspondent banking networks have been built over a century. SWIFT messaging standardized how institutions communicate across borders. When dLocal, Thunes, or Airwallex built their platforms, they were layering technology on top of banking rails and payment systems that already existed in most markets. They could aggregate local payment methods because those methods were regulated, documented, and accessible through established partnerships. Scale was a matter of integration work, not building net-new infrastructure.

Stablecoin on/off ramps don't have that luxury. The liquidity providers themselves are different. Traditional cross-border payments are powered by banks with deep balance sheets and access to interbank FX markets. Stablecoin on/off ramps are built by fintechs, each forging local banking relationships market by market. Each provider needs a banking partner willing to handle crypto-to-fiat conversion, and those relationships are hard-won and jurisdiction-specific. A bank in Brazil that's comfortable with stablecoin settlement may have a completely different cost structure than one in Mexico. Regulatory frameworks differ even within the same region: what's licensed and compliant in Colombia may carry different compliance overhead in Argentina. Liquidity pools are local, built on demand patterns that don't transfer even between neighboring markets.

These relationships are jurisdiction-specific. They're also fragile. A traditional correspondent banking relationship has decades of regulatory precedent, standardized compliance frameworks, and institutional momentum behind it. A bank's relationship with a stablecoin off-ramp provider has none of that. Banks are still developing their risk appetite for crypto-to-fiat flows. Regulatory guidance is still evolving. A bank that's processing stablecoin settlements today might decide next quarter that the compliance burden isn't worth it — or get pressure from a correspondent banking partner to stop. When that happens, the provider doesn't gradually become less competitive. A corridor that was live yesterday can be offline tomorrow.

Traditional payment providers have different cost bases in different markets too. But traditional FX liquidity is deep and consolidated enough that a single well-chosen provider can deliver competitive rates across most of your corridors, with the operational stability to back it up. The underlying infrastructure has converged over decades, so the cost structure differences between providers are marginal, and the reliability differences are negligible.

That's not the case in stablecoins — at least not today. The liquidity is local by design. Each provider's pricing is a function of jurisdiction-specific banking relationships, licenses, and demand patterns. A bank in Brazil that handles crypto-to-fiat conversion has no bearing on what a bank in Argentina charges for the same service. Even within the same region, top-ranked providers in one corridor sit at the bottom in the next — same continent, completely different liquidity pools. And the same factors that create pricing dispersion create operational risk: the more jurisdiction-specific and hard-won the banking relationship, the more fragile it is.

The data maps directly to this structure. Where local banking infrastructure is more mature, dispersion narrows: BRL at 65 bps. Where banking partners willing to handle stablecoin settlement are scarce, dispersion explodes: GHS at 575 bps. Same asset class, same underlying stablecoin, completely different local economics. Wide pricing gaps and provider disruptions stem from the same root: too few willing banking partners.

Will this improve over time? Some of it will. More banks will get comfortable with stablecoin settlement. Regulatory frameworks will mature. Liquidity pools will deepen in the corridors with enough demand. But traditional payments took decades of correspondent banking evolution and trillions in nostro account pre-funding before the liquidity consolidated to the levels you see today. Stablecoin infrastructure is years into that journey, not decades. If you're building stablecoin payment flows today — not in 2035 — the liquidity is fragmented, the optimal provider shifts corridor by corridor, reliability varies widely, and the market rewards those connected to multiple providers.

The Skyscanner Problem

In 2003, three friends sat in a London pub and sketched an idea on a beer mat. The travel industry was still dominated by traditional travel agencies. If you wanted to compare flight prices, you called airlines individually or visited their websites one by one. You got a price, and unless you were willing to spend hours checking alternatives, you had no way to know if it was competitive.

Skyscanner changed that by showing every airline's price for the same route, side by side, in seconds. But it didn't stop at visibility. You could see the prices, pick the best option, and Skyscanner routed you straight through to complete the booking. Compare, select, and execute in one flow. The prices themselves didn't change. What changed was that travelers could finally see what was out there and act on it.

Skyscanner saved you money, yes. But it also made you harder to strand. If your preferred airline cancelled a flight, raised prices, or dropped a route, you had alternatives right there. You were never locked in to a single carrier. The optionality was the product — and it doubled as your disaster recovery plan.

The parallel to stablecoin on/off ramps is almost exact.

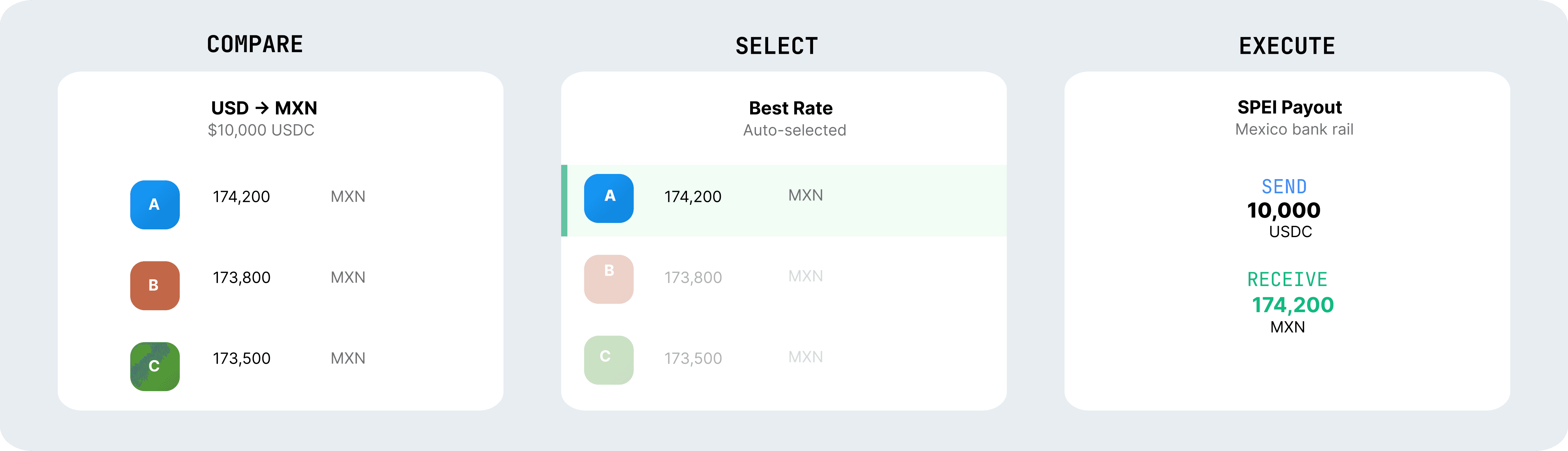

Today, most companies entering stablecoin payments pick a provider, get quoted a rate, and have no way to benchmark it. There's no Bloomberg terminal for stablecoin FX. No standardized mid-market rate. You're operating in a market where the spread between providers ranges from 6 to 575 basis points depending on the corridor, and you can't see any of it. You get a rate, have no way to know if it's the best or worst available, and won't find out until a competitor shows up with tighter pricing. Worse, you've built your entire payment flow on that one provider — so even if you wanted to switch, the integration cost and migration risk make it painful.

In traditional payments, this problem was solved decades ago. If your provider quoted you an FX rate on a USD-to-EUR corridor, you could check mid-market in seconds and know if you were getting a fair deal. The infrastructure for FX benchmarking, rate comparison, and provider evaluation exists and is mature. EU regulators are even pushing PSPs toward standardized disclosure of FX markups against a neutral benchmark.

None of that exists yet for stablecoin FX.

The companies that get multi-provider visibility first win three ways: on cost, on resilience, and on independence. When you can compare rates across providers for the same corridor in real time and route through the best one, you stop accepting whatever your single provider quotes you. And when a provider has an outage, loses a banking partner, or degrades in a corridor, you don't scramble for a workaround. You reroute. Compare, select, and execute the payment through the best available provider in one flow — and if something breaks, shift to the next one automatically.

This isn't about "aggregation." Aggregation implies a middleman wrapping and reselling someone else's rate with added markup. This is about orchestration: seeing all available rates across a corridor, routing to the best one, executing the full payment flow through a single platform — and never depending on a single rail to stay live.

What This Means for Your Business

If you're entering stablecoin payments with a single-provider strategy, you're making two bets at once. First, that one provider will have the best rate in every corridor you operate in, every time you transact. Second, that they'll stay operational, maintain their banking relationships, and continue performing — in every market, indefinitely. The data says the first bet is bad. The maturity of the market says the second one is risky.

No single provider consistently offered the best rate across the corridors we tested. Even within LatAm, the winners shifted from corridor to corridor. The best provider in Brazil was not the best in Colombia, which was not the best in Argentina. And even within a single corridor, the rankings shift over time. Today's best provider in Brazil may not be next month's.

On pricing alone, the cost of getting this wrong is significant. At $5M monthly volume, the blended annual cost of routing through the wrong provider is $1.28M. In high-dispersion corridors like GHS or ARS, it's multiples of that.

But the operational exposure may be worse. What happens when your single provider loses their banking partner in a key corridor? When they face a regulatory hold? When they promised settlement in 24 hours and it takes 72? In traditional payments, these are inconveniences — you have established escalation paths, contractual SLAs backed by decades of precedent, and providers with the balance sheet depth to absorb disruptions. In stablecoin payments, with younger providers, evolving regulations, and fragile local banking relationships, a single-provider dependency is a single point of failure with no safety net.

Multi-provider orchestration is more than a cost optimization. It's a business continuity strategy — and in practice, the only viable disaster recovery architecture for stablecoin payments today. If one provider degrades, routing shifts. If a corridor goes dark with one partner, another picks it up. There's no waiting for a provider to restore service, no emergency integration sprint to onboard a replacement. The failover is already live, already tested, already routing volume. You maintain independence from any single vendor's roadmap, pricing decisions, or operational limitations.

In payments, customers are price-sensitive. They compare rates, and they move. If a competing PSP has multi-provider visibility and you're still routing through a single provider, they're structurally cheaper in every corridor you share. But they're also more reliable — and when your customers' payments fail because your single provider had a bad day, they won't wait for you to fix it.

The market is moving toward multi-provider orchestration. The question isn't whether this matters to your business. It's whether your competitors get there first.

Methodology

All data in this analysis comes from USDC sell rate quotes collected across 10 licensed stablecoin on/off ramp providers in the Borderless network between December 2025 and February 2026. Rates were captured at identical timestamps and notional amounts to ensure like-for-like comparison. Each corridor had between 3 and 5 active providers quoting during the analysis window.

Dispersion is measured as the gap between each provider's median sell rate over the full period, expressed in basis points: (best - worst) / midpoint x 10,000. Dollar impact is calculated as: volume x (best_rate - worst_rate) / best_rate. Statistical outliers were excluded using a Hampel filter (z > 6) and provider divergence greater than 10% from consensus mid-rate.

All providers are anonymized. This analysis measures cross-provider sell rate dispersion (the gap between different providers quoting the same corridor), not the buy-sell spread within a single provider.

You know how to move money across borders. You've built payment flows across dozens of corridors, benchmarked providers on total cost and settlement speed, and optimized routing for every market you operate in. You can compare the all-in cost of a payment through one rail versus another in seconds. Cross-border payments are a margin game, and you've spent years learning how to win it.

Stablecoin on/off ramps are a much less mature market. The provider landscape is fragmented, pricing is opaque, and the benchmarking tools that traditional payments teams take for granted are still catching up. Pricing opacity is just the start. The providers themselves are younger, less battle-tested, and building on banking relationships far more fragile than anything on traditional rails. If you're a payments company expanding into stablecoins, the same disciplines apply, but the provider risk profile is nothing like what you're used to.

The Market You Know vs. the Market You're Entering

Traditional cross-border payments run on infrastructure that's been built, rebuilt, and optimized over decades. At the foundation, you have correspondent banking: networks of nostro and vostro accounts where banks pre-fund foreign currency balances so they can settle transactions on each other's behalf. On top of that, you have the networks and platforms that move money at scale. Mastercard Move reaches 10 billion endpoints across 200 countries. Thunes connects over 7 billion mobile wallets and bank accounts across 130 countries. dLocal processes over $9 billion per quarter across 40+ emerging markets. Airwallex handles global FX and payments infrastructure for businesses across 150+ countries.

These are mature rails. If you're a PSP operating in this world, the playbook is straightforward. You pick a provider, commit volume, and negotiate your pricing down. The more volume you bring, the tighter your basis points. It works because the underlying liquidity is deep enough and consolidated enough that a single well-chosen partner can offer competitive rates across most of your corridors. These providers are also stable. Redundant banking relationships. Regulatory frameworks they've operated under for years. Uptime measured in nines. When you commit volume to a Thunes or a dLocal, you're not worried about whether they'll still be able to settle in Brazil next quarter.

Stablecoin on/off ramps work differently.

There's no equivalent infrastructure. Instead, there are dozens of regional on-ramp and off-ramp providers, each licensed in specific jurisdictions, each with different banking relationships, and each pricing their FX conversion independently. A provider with deep local bank partnerships in Brazil may have excellent BRL rates but much weaker liquidity in Mexico. Another might offer tight spreads in Kenya but charge a premium in Nigeria.

The pricing fragments. So does the reliability. These are younger companies, and the banking relationships they depend on can break. A local bank that's comfortable handling crypto-to-fiat today might pull back tomorrow — after a regulatory shift, a compliance review, or simply a change in risk appetite at the bank. When that happens, the provider doesn't reprice. The corridor goes dark. In traditional payments, losing a banking partner is a disruption you manage. In stablecoin off-ramps, your payments in that market stop. No notice. No fallback.

And because the market is still in its land-grab phase, providers are competing aggressively for early volume. They'll promise coverage, rates, and capabilities to get you signed. Some will deliver. Some won't. The gap between what's on the pitch deck and what's in production can be significant — and you won't always find out until you're live, volume is flowing, and switching costs are real.

In traditional payments, your disaster recovery plan for a provider outage is straightforward - you have secondary routes, established failover procedures, and providers with the operational depth to recover quickly. In stablecoin payments, if your single provider goes down in a corridor, there's no secondary route. You don't have a warm standby. You have a phone call and a scramble.

The traditional playbook of committing volume to a single provider doesn't solve the problem. The liquidity is too fragmented for any one partner to be consistently competitive across your corridors. And the operational risk of depending on a single, less mature provider — with jurisdiction-specific banking relationships that could change at any time — is a bet most payments teams wouldn't accept on traditional rails. Why accept it here?

We wanted to quantify just how wide the pricing gaps are. So we ran the numbers.

The Data

We analyzed USDC sell rate quotes across 10 licensed providers over a three-month window. Eight corridors: four in Latin America (BRL, MXN, ARS, COP) and four in Africa (GHS, KES, NGN, ZAR). All rates captured at the same timestamps, same notional amounts, providers anonymized.

The median cross-provider dispersion across all eight corridors was 176 basis points. For a PSP routing $5M per month through stablecoin off-ramps, that translates to over $1.2 million per year in avoidable cost from provider selection alone.

Corridor | Spread (bps) | @ $5M/mo | @ $25M/mo | @ $100M/mo |

|---|---|---|---|---|

USDC→GHS | 575 | $3.35M | $16.77M | $67.07M |

USDC→ARS | 394 | $2.32M | $11.59M | $46.37M |

USDC→NGN | 191 | $1.14M | $5.68M | $22.73M |

USDC→MXN | 186 | $1.11M | $5.53M | $22.12M |

USDC→KES | 165 | $0.98M | $4.91M | $19.63M |

USDC→COP | 152 | $0.91M | $4.54M | $18.15M |

USDC→BRL | 65 | $0.39M | $1.96M | $7.82M |

USDC→ZAR | 6 | $0.04M | $0.18M | $0.73M |

Blended avg | 176 | $1.28M | $6.39M | $25.58M |

Per-corridor figures assume full volume in that corridor. Blended average assumes equal distribution across all eight. See Methodology for details.

The range tells its own story. In South Africa, providers largely agree on pricing: 6 bps of dispersion. In Ghana, they don't: 575 bps, nearly a hundred times wider. Even within the same continent, the variation is dramatic. Nigeria (191 bps) looks nothing like South Africa (6 bps). Colombia (152 bps) looks nothing like Brazil (65 bps).

Pricing dispersion is what we can put numbers on. Reliability, settlement consistency, and corridor uptime vary at least as much — they're just harder to put in a table. The corridors with the widest pricing gaps are the same ones where banking relationships are thinnest and providers are most likely to hit disruptions. High dispersion is a maturity signal, not just a pricing one.

But the most important finding isn't the size of the gaps. It's that no single provider wins everywhere.

No single provider consistently offered the best rate across corridors. The best provider in Brazil was different from the best in Colombia, which was different from the best in Argentina. Same story in Africa: the provider with the best rate in Ghana ranked dead last in Kenya. Even a PSP focused on a single region still faces a market where the optimal provider shifts corridor by corridor.

This means static provider routing — picking one partner and sending all volume through them — leaves money on the table regardless of your geographic focus. It also concentrates risk. When your single provider has an outage, loses a banking relationship, or faces regulatory action in a market you depend on, there's no plan B. No failover. No continuity. No single provider is bad. But the market rewards breadth — better pricing, built-in redundancy, and the leverage of not depending on a single vendor's fate. The PSP with that breadth is cheaper, more resilient, and harder to knock offline in every corridor they compete in.

Why the Dispersion Exists

If you're coming from traditional payments, your instinct is to assume this is a temporary inefficiency. That the market will consolidate, a few winners will emerge, and spreads will tighten to the levels you're used to. Eventually, some of that will happen. But the fragmentation in stablecoin on/off ramps isn't a bug. It's structural, and it changes how you approach the market.

In traditional cross-border payments, consolidation happened because the underlying infrastructure allowed it. Correspondent banking networks have been built over a century. SWIFT messaging standardized how institutions communicate across borders. When dLocal, Thunes, or Airwallex built their platforms, they were layering technology on top of banking rails and payment systems that already existed in most markets. They could aggregate local payment methods because those methods were regulated, documented, and accessible through established partnerships. Scale was a matter of integration work, not building net-new infrastructure.

Stablecoin on/off ramps don't have that luxury. The liquidity providers themselves are different. Traditional cross-border payments are powered by banks with deep balance sheets and access to interbank FX markets. Stablecoin on/off ramps are built by fintechs, each forging local banking relationships market by market. Each provider needs a banking partner willing to handle crypto-to-fiat conversion, and those relationships are hard-won and jurisdiction-specific. A bank in Brazil that's comfortable with stablecoin settlement may have a completely different cost structure than one in Mexico. Regulatory frameworks differ even within the same region: what's licensed and compliant in Colombia may carry different compliance overhead in Argentina. Liquidity pools are local, built on demand patterns that don't transfer even between neighboring markets.

These relationships are jurisdiction-specific. They're also fragile. A traditional correspondent banking relationship has decades of regulatory precedent, standardized compliance frameworks, and institutional momentum behind it. A bank's relationship with a stablecoin off-ramp provider has none of that. Banks are still developing their risk appetite for crypto-to-fiat flows. Regulatory guidance is still evolving. A bank that's processing stablecoin settlements today might decide next quarter that the compliance burden isn't worth it — or get pressure from a correspondent banking partner to stop. When that happens, the provider doesn't gradually become less competitive. A corridor that was live yesterday can be offline tomorrow.

Traditional payment providers have different cost bases in different markets too. But traditional FX liquidity is deep and consolidated enough that a single well-chosen provider can deliver competitive rates across most of your corridors, with the operational stability to back it up. The underlying infrastructure has converged over decades, so the cost structure differences between providers are marginal, and the reliability differences are negligible.

That's not the case in stablecoins — at least not today. The liquidity is local by design. Each provider's pricing is a function of jurisdiction-specific banking relationships, licenses, and demand patterns. A bank in Brazil that handles crypto-to-fiat conversion has no bearing on what a bank in Argentina charges for the same service. Even within the same region, top-ranked providers in one corridor sit at the bottom in the next — same continent, completely different liquidity pools. And the same factors that create pricing dispersion create operational risk: the more jurisdiction-specific and hard-won the banking relationship, the more fragile it is.

The data maps directly to this structure. Where local banking infrastructure is more mature, dispersion narrows: BRL at 65 bps. Where banking partners willing to handle stablecoin settlement are scarce, dispersion explodes: GHS at 575 bps. Same asset class, same underlying stablecoin, completely different local economics. Wide pricing gaps and provider disruptions stem from the same root: too few willing banking partners.

Will this improve over time? Some of it will. More banks will get comfortable with stablecoin settlement. Regulatory frameworks will mature. Liquidity pools will deepen in the corridors with enough demand. But traditional payments took decades of correspondent banking evolution and trillions in nostro account pre-funding before the liquidity consolidated to the levels you see today. Stablecoin infrastructure is years into that journey, not decades. If you're building stablecoin payment flows today — not in 2035 — the liquidity is fragmented, the optimal provider shifts corridor by corridor, reliability varies widely, and the market rewards those connected to multiple providers.

The Skyscanner Problem

In 2003, three friends sat in a London pub and sketched an idea on a beer mat. The travel industry was still dominated by traditional travel agencies. If you wanted to compare flight prices, you called airlines individually or visited their websites one by one. You got a price, and unless you were willing to spend hours checking alternatives, you had no way to know if it was competitive.

Skyscanner changed that by showing every airline's price for the same route, side by side, in seconds. But it didn't stop at visibility. You could see the prices, pick the best option, and Skyscanner routed you straight through to complete the booking. Compare, select, and execute in one flow. The prices themselves didn't change. What changed was that travelers could finally see what was out there and act on it.

Skyscanner saved you money, yes. But it also made you harder to strand. If your preferred airline cancelled a flight, raised prices, or dropped a route, you had alternatives right there. You were never locked in to a single carrier. The optionality was the product — and it doubled as your disaster recovery plan.

The parallel to stablecoin on/off ramps is almost exact.

Today, most companies entering stablecoin payments pick a provider, get quoted a rate, and have no way to benchmark it. There's no Bloomberg terminal for stablecoin FX. No standardized mid-market rate. You're operating in a market where the spread between providers ranges from 6 to 575 basis points depending on the corridor, and you can't see any of it. You get a rate, have no way to know if it's the best or worst available, and won't find out until a competitor shows up with tighter pricing. Worse, you've built your entire payment flow on that one provider — so even if you wanted to switch, the integration cost and migration risk make it painful.

In traditional payments, this problem was solved decades ago. If your provider quoted you an FX rate on a USD-to-EUR corridor, you could check mid-market in seconds and know if you were getting a fair deal. The infrastructure for FX benchmarking, rate comparison, and provider evaluation exists and is mature. EU regulators are even pushing PSPs toward standardized disclosure of FX markups against a neutral benchmark.

None of that exists yet for stablecoin FX.

The companies that get multi-provider visibility first win three ways: on cost, on resilience, and on independence. When you can compare rates across providers for the same corridor in real time and route through the best one, you stop accepting whatever your single provider quotes you. And when a provider has an outage, loses a banking partner, or degrades in a corridor, you don't scramble for a workaround. You reroute. Compare, select, and execute the payment through the best available provider in one flow — and if something breaks, shift to the next one automatically.

This isn't about "aggregation." Aggregation implies a middleman wrapping and reselling someone else's rate with added markup. This is about orchestration: seeing all available rates across a corridor, routing to the best one, executing the full payment flow through a single platform — and never depending on a single rail to stay live.

What This Means for Your Business

If you're entering stablecoin payments with a single-provider strategy, you're making two bets at once. First, that one provider will have the best rate in every corridor you operate in, every time you transact. Second, that they'll stay operational, maintain their banking relationships, and continue performing — in every market, indefinitely. The data says the first bet is bad. The maturity of the market says the second one is risky.

No single provider consistently offered the best rate across the corridors we tested. Even within LatAm, the winners shifted from corridor to corridor. The best provider in Brazil was not the best in Colombia, which was not the best in Argentina. And even within a single corridor, the rankings shift over time. Today's best provider in Brazil may not be next month's.

On pricing alone, the cost of getting this wrong is significant. At $5M monthly volume, the blended annual cost of routing through the wrong provider is $1.28M. In high-dispersion corridors like GHS or ARS, it's multiples of that.

But the operational exposure may be worse. What happens when your single provider loses their banking partner in a key corridor? When they face a regulatory hold? When they promised settlement in 24 hours and it takes 72? In traditional payments, these are inconveniences — you have established escalation paths, contractual SLAs backed by decades of precedent, and providers with the balance sheet depth to absorb disruptions. In stablecoin payments, with younger providers, evolving regulations, and fragile local banking relationships, a single-provider dependency is a single point of failure with no safety net.

Multi-provider orchestration is more than a cost optimization. It's a business continuity strategy — and in practice, the only viable disaster recovery architecture for stablecoin payments today. If one provider degrades, routing shifts. If a corridor goes dark with one partner, another picks it up. There's no waiting for a provider to restore service, no emergency integration sprint to onboard a replacement. The failover is already live, already tested, already routing volume. You maintain independence from any single vendor's roadmap, pricing decisions, or operational limitations.

In payments, customers are price-sensitive. They compare rates, and they move. If a competing PSP has multi-provider visibility and you're still routing through a single provider, they're structurally cheaper in every corridor you share. But they're also more reliable — and when your customers' payments fail because your single provider had a bad day, they won't wait for you to fix it.

The market is moving toward multi-provider orchestration. The question isn't whether this matters to your business. It's whether your competitors get there first.

Methodology

All data in this analysis comes from USDC sell rate quotes collected across 10 licensed stablecoin on/off ramp providers in the Borderless network between December 2025 and February 2026. Rates were captured at identical timestamps and notional amounts to ensure like-for-like comparison. Each corridor had between 3 and 5 active providers quoting during the analysis window.

Dispersion is measured as the gap between each provider's median sell rate over the full period, expressed in basis points: (best - worst) / midpoint x 10,000. Dollar impact is calculated as: volume x (best_rate - worst_rate) / best_rate. Statistical outliers were excluded using a Hampel filter (z > 6) and provider divergence greater than 10% from consensus mid-rate.

All providers are anonymized. This analysis measures cross-provider sell rate dispersion (the gap between different providers quoting the same corridor), not the buy-sell spread within a single provider.

Global Stablecoin Orchestration Network

Borderless Innovations Labs Inc. (Borderless) is a technology and smart contract development company. Borderless in not a broker-dealer or financial institution and does not engage any conduct or transactions requiring such registration. All financial products are offered by and through financial institutions directly. Borderless does not make any recommendation for the purchase or sale of digital assets. Our products and services are offered in limited jurisdictions so please contact our partnerships team for further information and refer to our Terms of Services.

Global Stablecoin Orchestration Network

Borderless Innovations Labs Inc. (Borderless) is a technology and smart contract development company. Borderless in not a broker-dealer or financial institution and does not engage any conduct or transactions requiring such registration. All financial products are offered by and through financial institutions directly. Borderless does not make any recommendation for the purchase or sale of digital assets. Our products and services are offered in limited jurisdictions so please contact our partnerships team for further information and refer to our Terms of Services.

Global Stablecoin Orchestration Network

Borderless Innovations Labs Inc. (Borderless) is a technology and smart contract development company. Borderless in not a broker-dealer or financial institution and does not engage any conduct or transactions requiring such registration. All financial products are offered by and through financial institutions directly. Borderless does not make any recommendation for the purchase or sale of digital assets. Our products and services are offered in limited jurisdictions so please contact our partnerships team for further information and refer to our Terms of Services.